The two problems that cause most BI underinsurance

Business interruption insurance is designed to replace your income if you can’t trade following an insured event. In practice, most BI policies don’t fully achieve this — not because the policy contains exclusions that apply, but because of how the cover was structured in the first place.

There are two recurring problems: an incorrectly calculated sum insured, and an indemnity period that doesn’t reflect how long recovery actually takes.

Both problems are invisible until a claim occurs. By then, they’re irreversible.

The sum insured problem: insurance gross profit vs accounting gross profit

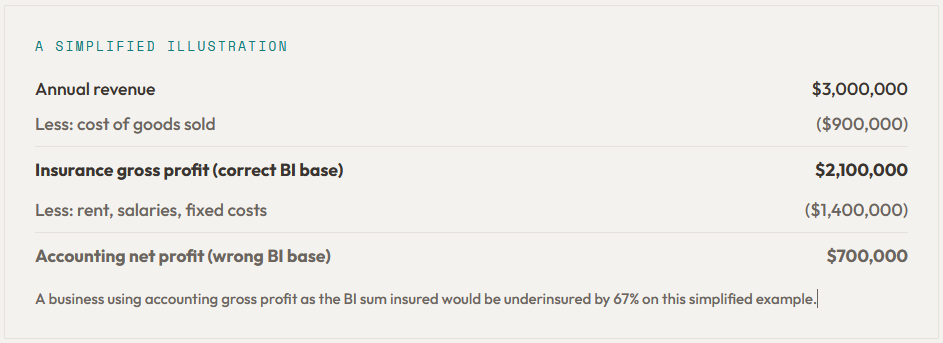

BI cover is structured around “gross profit” — but the insurance definition of gross profit is different from what appears on your profit and loss statement.

Insurance gross profit is calculated as: Revenue, less the costs that would genuinely stop if you stopped trading. These are variable costs — raw materials, cost of goods sold, direct production labour, freight on goods sold.

Fixed costs that continue regardless of whether you’re trading — rent, fixed salaries, loan repayments, insurance premiums, lease costs — are included in insurance gross profit, because you still have to pay them even when you’re not earning.

The common mistake: business owners calculate their BI sum insured using the gross profit that appears on their P&L, which has already deducted fixed costs. This produces a number that significantly understates the correct insured amount.

The indemnity period problem

The indemnity period is the maximum length of time the policy will pay for loss of income. Standard policies default to 12 months. The question is: how long would it actually take your business to return to full trading capacity following a total loss?

For most businesses, the honest answer is not 12 months:

- Manufacturer with specialist equipment: Lead times for machinery sourcing, import, delivery, installation, and recommissioning can run to 18–36 months

- Retail or hospitality: A fit-out rebuild, council approval, and staff rebuild typically runs 9–18 months

- Professional services: Data recovery, system rebuild, client re-engagement — 6–12 months depending on the nature of the loss

If your indemnity period expires before you’ve returned to full trading, the remaining loss is uninsured. The business absorbs it.

What actually triggers BI — and what doesn’t

BI only activates following a covered event under your policy. If the event that caused the interruption isn’t covered, BI doesn’t trigger. Three common gaps:

No contingent BI

A key supplier is disrupted — fire at their premises, flood at the warehouse. Your production stops. Standard BI covers your own premises loss, not a supply chain failure. A contingent BI extension covers loss arising from a disruption to a named supplier or customer.

No utilities extension

Power outage from a utilities disruption — not caused by damage to your own premises — takes you offline. Standard property-based BI typically doesn’t trigger unless a utilities extension is included.

Cyber BI is separate

A ransomware attack takes your systems down. Standard property-based BI doesn’t trigger — cyber is a separate cause. Cyber BI is a component of a standalone cyber policy, not a property policy extension.

How to set it correctly

The correct BI structure: take your annual revenue, deduct only costs that genuinely vary with revenue, set the result as your insured sum. Choose an indemnity period that reflects what full operational recovery actually looks like for your specific business. Review both annually, because revenue changes.

These are not complicated calculations. They’re just not the calculations most businesses do at renewal.